Bank of Ghana (BoG): The decline in Ghana’s inward remittances has been validated by the Bank of Ghana that the newly licensed MTOs and 11 Fintech Companies have withheld approximately GH¢18 billion (US$ 3 billion) in 2022 and GH¢57 billion (US$ 5 billion) in 2023 at the expense of the country’s foreign currency reserves. The country has lost approximately US$ 8 billion in the past two years, which could have been used to shore up the persistent depreciation of the local currency against the major trading currencies.

First, the bone of contention has never been about Ghana’s declining remittance but rather the increasing under-reporting of inward remittances. In fact, the central bank has consistently failed to address the gap or discrepancies between the World Bank data on inward remittances and that of the 23 authorised dealer bank data for the period between 2019 to 2023, as well as inflows passing Fintech companies captured in its 2023 annual report. The key question is, why is there a huge gap between BoG’s data reported by the Auditor General and that recorded by the World Bank?

The statement from the Bank of Ghana that the inward remittance guidelines mandate Fintech companies to work with partner local banks and Fintech companies have no authority whatsoever to hold remittance proceeds outside of the Ghanaian banking system is misleading. The Governor in the 2023 Annual Report told the entire nation that Fintech companies received GH¢22 billion (US$ 3 billion) in 2022 and GH¢57 billion (US$ 5 billion) respectively.

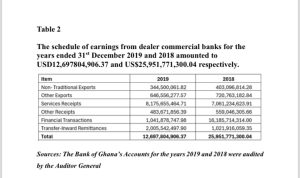

Where were these two foreign exchanges in respect of the inward remittances held? The US$ 8 billion equivalent of GHS 79 billion held was not reflected in the Auditor-General’s Report on the Consolidated Statements of Foreign Exchange Receipts: Schedule of inward remittance from 23 authorized dealer commercial banks for 2022 and 2023 (First Half) respectively. The Auditor-General’s report on the Consolidated Statements of Foreign Exchange Receipts: Schedule of inward remittances from the 23 Authorized dealer commercial banks recorded US$ 2.1 billion in 2022 while the half year of 2023 recorded US$ 1.28 billion. Where is the foreign exchange in respect of the Fintech companies’ inward remittances which were received with the total GHS 79 billion equivalent of US$ 8 billion?

Furthermore, how much did the Fintech Companies receive for 2019; 2020, and 2021, and how did the bank capture the foreign exchange component? I would be grateful if the Bank of Ghana could address the gaps between the World Bank data and the Auditor General’s report inclusive of the Fintech companies in the inward remittances space since 2019.

For the avoidance of doubt, the central bank must tell the entire nation which of the authorised dealer banks benefited the foreign exchange in respect of inward remittances from the Fintech companies to the tune of US$3 billion and US$5 billion respectively in 2022 and 2023 respectively. The Governor must indicate which local partner banks received foreign exchanges concerning the Fintech companies’ remittances inflows. As stated by the Bank of Ghana’s press release which local partner banks benefited from the Fintech transactions and how did local partner banks treat the remittance inflows in their books?

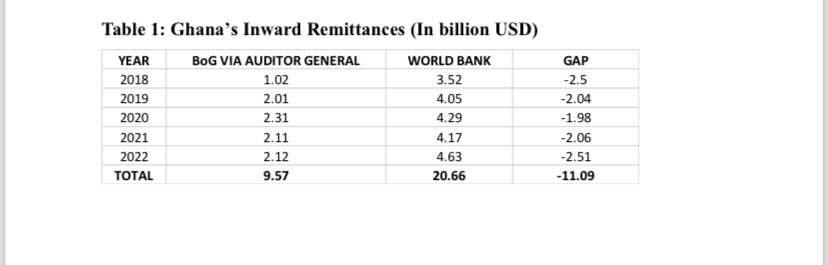

Second, the Bank of Ghana’s data showed that the country recorded US$ 2 billion in 2019; US$2.3 billion in 2020; US$ 2.1 billion in 2021; US$ 2.1 billion in 2022, and half year of 2023 US$1.28 billion from inward remittances.

However, the World Bank data has shown a consistent growth in remittance inflows for the period under review. World Bank data on remittance inflows showed that Ghana received US$ 4.1billion in 2019; increased marginally to US$ 4.3 billion in 2020; further increased to US$ 4.5billion in 2021; improved slightly to US$ 4.7 billion in 2022 but declined to US$ 4.6 billion in 2023 according to the World Bank’s new global data on inward remittances released on 25/06/2024 as against earlier data released in March 2024.

So, Bank of Ghana’s own data given to the Auditor General on inward remittances couldn’t capture the claimed consistent growth or is the central bank relying on the World Bank data which is completely at variance with its data? The bank must be clear on which data it is using to make this claim as both sources have different figures.

The claim by the Bank of Ghana that inward remittances have seen consistent growth is inaccurate as its data revealed that remittance inflows into the country have stagnated over the past five years. The World Bank data on remittance inflows for the period between 2019 to 2022 was US$ 20.66 billion while the Bank of Ghana data on inward remittance was US$ 9.57 billion leaving a gap of US$12.45 billion. This is shown in the table 1 below:

Third, the Bank of Ghana’s rejoinder on inward remittances did not address the thrust of the paper that suggested that the country lost US$3 billion (GH¢18 billion) and US$5 billion (GH¢57 billion) through the operations of Fintech companies in 2022 and 2023 respectively. From the Bank of Ghana’s data on remittance inflows for 2022 and 2023, the foreign exchange from these institutions could not be traced to the Auditor-General’s Report on the Consolidated Statements of Foreign Exchange Receipts: Schedule of inward remittance from 23 authorised dealer commercial banks for 2022 and 2023 respectively.

However, from the above data it could be deduced that these funds had been externalised via digital transfers from other countries.

The foreign exchange in respect of Fintech companies’ remittance inflows does not reflect on the Auditor-General’s Report on the Consolidated Statements of Foreign Exchange Receipts: Schedule of earnings from 23 authorized dealer commercial banks at the period for both 2022 and half year of 2023. This has confirmed and validated the statement that the remittance inflows have been externalised by the 11 licensed Fintech Companies. The externalisations deny the interbank market of Ghana’s foreign exchange liquidity, hence the difficulty in sourcing forex to support domestic economic activities transparently.

This has been the practice in Nigeria, according to Hon. Taiwo Oyedele, the Chairman of the Presidential Committee on Fiscal Policy and Tax Reforms recently revealed that 10% of the US$20 billion in diaspora remittances for 2023 made it to the Nigerian foreign exchange market and 90% of inward remittance have externalised by Fintech companies. This will be in breach of the Foreign Exchange Act 2006 Act 723 contrary to the response by the Bank of Ghana’s statement on the inward remittances.

The 11 Fintech companies licensed since 2019 use digital apps to calculate market rates to credit Cedis here in Ghana without bringing corresponding foreign exchange in respect of inward remittances flows. Has the foreign exchange in respect of remittance inflows been eternalized in breach of the Foreign Exchange Act 2006 Act 723? Studies from developing countries clearly show the central banks are suffering from externalization since the introduction of Fintech companies into the remittance inflows space for example Nigeria is a clear case.

Remittances routed through formal channels are generally traceable through the formal financial system balances and recorded the national balances and forex accounts, increasing the official reserves. Remittance inflows remain a stable and sustainable source of foreign exchange earnings too huge to be ignored.

Fourth, another lack of understanding exhibited by the Bank of Ghana on the failure to appreciate the implications of the International Accounting Standard practices of IAS 21 on the Bank of Ghana’s failure to indicate the foreign exchange equivalent of the GH¢22 billion and GH¢57 billion remittance receipts by the Fintech companies had proved to be the flaw in the Bank of Ghana 2023 annual report published in June 2024 which the Bank of Ghana’s rejoinder failed to address the non-compliance of the IAS 21. IAS 21 states the Effects of Changes in Foreign Exchange Rates guide to determine the functional currency of an entity under International Financial Reporting Standards (IFRS).

The standard also prescribes how to include foreign currency transactions and foreign operations in the financial statements of an entity and how to translate financial statements from the entity’s functional currency into its presentation currency. This factsheet will delve into determining an entity’s functional currency, determining the functional currency of a foreign operation, and dealing with a change in the said functional currency.

IAS 21 on “The Effects of Changes in Foreign Exchange Rates” outlines how to account for foreign currency transactions and operations in financial statements, and also how to translate financial statements into a presentation currency. An entity is required to determine a functional currency (for each of its operations if necessary) based on the primary economic environment in which it operates and generally records foreign currency transactions using the spot conversion rate to that functional currency.

Fifth, the Bank of Ghana’s response that data on inward remittances captured was Net position basis clearly showed that lack of understanding of how the central bank captures inward remittances under the Sixth Edition of the IMF Balance of Payments and International Investment Position Manual (BPM6). Bank of Ghana must note that information transactions under BPM6 are not ‘Net’. All transactions recorded in the Bank of Ghana must comply with the IMF Balance of Payments and International Investment Position Manual (BPM6) 6th Edition.

Remittance data is reported by central banks’ balance of payments compilers based on the IMF BMP6 and RCG remittance framework, which were released in 2009. The Balance of Payments and International Investment Position Manual, 6th edition (BPM6), guides IMF member countries on the compilation of BOP and IIP statistics.

The Manual also aims to enhance the comparability of data across countries through the promotion of standards adopted internationally. The BPM6 manual was released in 2009 as an update to BPM5 to reflect changes that had taken place in the international economic and financial environment and to coincide with the update of the System of National Account SNA from SNA 1993 to SNA 2008.

The Bank of Ghana’s statement that remittance inflows are recorded is incorrect. It is false to state that the data captured shows ‘Net Position’ as claimed by its Director of Communication, Bernard Otabil.

The under-listed data for 2018 and 2019 confirmed the various transactions have all been grossed up but not the Net position.

Policy Recommendation:

First, specifically, the Bank of Ghana should not only focus on licensing the Fintech companies and the designing of policies to monitor and analyse the impact of remittance receipts, to develop retail digital systems and submission of regulatory returns and also to develop strategies to intermediate this foreign exchange through the formal banking system and channel them into productive investment such as international payment for goods and services.

Second, to prevent future occurrences, where the Fintech companies hold onto foreign exchange in respect of remittance inflows, the Bank of Ghana must acquire software or malware that could be linked to the various digital apps of the Fintech companies to track, trace, and capture all inward remittances and also Bank of Ghana could be part of a settlement arrangement with Fintech companies as done previously by the local banks that partnered Western Union, Money gram and Rio Money transfer systems. Bank of Ghana must implement a simple Middleware platform where all fintech companies’ digital apps could be connected to enable the Bank of Ghana to track and trace all remittance inflow settlements of the Fintech companies.

This could be done using APIs. Ethernet-APL is a technology that enables powerful and consistent digital communication in process automation from the sensor to the control level. Ethernet-APL has all the features required by a modern, future-proof network in process automation. This way, it should be possible for the Bank of Ghana to check for under- declaration or misreporting of foreign exchange into the country by the Fintech companies. This means that the Bank of Ghana will not need to rely on reporting by banks or the fintech companies themselves to know the foreign exchange volumes. This should also help the Bank of Ghana to deal with all manipulations by the Fintech companies.

Third, the Ministry of Finance and Bank of Ghana must ensure the Fintech companies in the international remittances space reimburse the Bank of Ghana’s Nostro-Accounts or authorised dealer commercial bank with all foreign exchange components of all foreign exchange accrued as it was previously done in the early 2000s and also in compliance with Foreign Exchange Act 2006 Act 723. Foreign exchange from inward remittances, for instance, could help to reduce the current account deficit and also help to stabilise the local currency against major trading currencies like US$, Euro, and UK Pound Sterling. The Bank of Ghana should be prepared to reconcile the Nostro Accounts of all Fintech companies. Bank of Ghana should commission some of the international audit firms to conduct forensic audits on all Fintech companies since 2019.

Fourth, with the innovation of new technologies such as digital apps of Fintech companies and digital currencies coming into mainstream finance, the Bank of Ghana and IMF should take a greater onus to improve its BPM6 and RCG remittance data framework. Firstly, to support developing countries like Ghana dependent on remittances rather than pointing out inaccuracies of current remittance data which are primarily due to BPM6 and RCG remittance frameworks having poorly constructed concepts, definitions, and data sources. Secondly, by defining and updating the underlying remittance transactions and their calculations to capture the on-ground realities of the remittance sector. Under BPM6 standard treatment, Remittances are mainly derived from two items in the BOP framework: income earned by workers in economies where they are not residents (compensation of employees) and personal transfers from residents of one economy to residents of another (IMF, 2008).

In other emerging economies like Sri Lanka, Bangladesh, and Pakistan, remittances have been the key pillars of foreign currency earnings providing a substantial cushion against the widening trade deficit and thereby enhancing the external sector resilience of the country. Being a major source of foreign exchange earnings, workers’ remittances have hovered around 80 percent of the annual trade deficit, on average, over the past two decades, and Fintech companies are required to submit all their foreign exchange holdings to the central bank.

Moreover, unlike many merchandise export categories, there is no import content involved in this source of foreign exchange earnings. Therefore, strengthening remittance inflows to the country brings several macroeconomic and socioeconomic benefits, mainly narrowing the current account deficit of Balance of Payments (BOP), supporting economic growth and stability of exchange rate as well as improving forex liquidity in the banking system.

Explore the world of impactful news with CitiNewsroom on WhatsApp!

Click on the link to join the Citi Newsroom channel for curated, meaningful stories tailored just for YOU: https://whatsapp.com/channel/0029VaCYzPRAYlUPudDDe53x

No spams, just the stories that truly matter! #StayInformed #CitiNewsroom #CNRDigital

{kind=link}